Informe de mercados

Sentimiento de mercado, por Iván Sdruvolini:

La jornada estuvo marcada por un renovado optimismo en torno a la inteligencia artificial y la tecnología. Las bolsas asiáticas registraron fuertes avances, lideradas por Corea del Sur, donde el mercado protagonizó una subida récord impulsada por el regreso de los inversores a los valores vinculados a la IA. El movimiento siguió a un importante rebote de los fabricantes de semiconductores en Wall Street, mientras los futuros estadounidenses también apuntaban al alza. En contraste, Japón mantuvo sin cambios los tipos de interés y el yen siguió bajo presión pese a las recientes intervenciones de las autoridades monetarias. En el ámbito corporativo, los resultados de las grandes tecnológicas ofrecieron señales mixtas. Amazon fue bien recibida gracias al crecimiento de su negocio de computación en la nube AWS, mientras Apple cayó tras advertir que la escasez de componentes afectará a sus ventas futuras. Microsoft continúa consolidándose como uno de los grandes beneficiarios del auge de la IA, mientras DeepSeek anunció planes para desarrollar un gigantesco centro de datos en Mongolia Interior. También surgieron nuevas preocupaciones sobre seguridad tecnológica después de que Anthropic revelara que varios de sus modelos lograron acceder a sistemas externos durante pruebas de ciberseguridad. En política internacional, Donald Trump anunció que una iniciativa liderada por Estados Unidos habría alcanzado un acuerdo para el desarme completo de Hamás y otros grupos armados en Gaza, así como para la creación de una nueva administración palestina. No obstante, los detalles y plazos de implementación todavía deben concretarse. Paralelamente, España desplegará al ejército en Ceuta tras una grave crisis migratoria en la frontera con Marruecos que dejó varias víctimas mortales. En Asia, China afrontó un deterioro de la actividad manufacturera, con el PMI oficial cayendo a 49,2 y entrando nuevamente en zona de contracción. Además, el país sufrió el deslizamiento de tierra más mortal en más de una década, con al menos 51 fallecidos. Japón anunció la creación de una nueva agencia nacional de inteligencia enfocada en seguridad nacional. En los mercados energéticos, el petróleo continuó corrigiendo ante la menor tensión entre Estados Unidos e Irán, aunque persisten los riesgos sobre el suministro global. Europa sigue preocupada por posibles interrupciones en el estrecho de Ormuz, que podrían dificultar el almacenamiento de gas de cara al invierno. Mientras tanto, la Reserva Federal mantuvo los tipos en el 3,50%-3,75%, aunque la división interna de sus miembros mantiene vivas las dudas sobre nuevas subidas si la inflación continúa mostrando resistencia. Con esto nos despedimos hasta septiembre con nuestro informe diario, esperamos que disfruten de las vacaciones.

Comentario de divisas, por Enrique Velasco:

Tras la intervención de ayer de Japón en el mercado de divisas para frenar la depreciación de su divisa, la reunión del BoJ ha servido para reforzar la percepción de que la normalización monetaria sigue avanzando. La entidad mantuvo los tipos de interés sin cambios, una decisión ampliamente descontada por el mercado, pero el tono del comunicado resultó algo más constructivo respecto a las perspectivas de inflación y crecimiento. Lo más relevante para el mercado de divisas es que el debate dentro del propio banco parece estar desplazándose gradualmente hacia cuándo volver a subir tipos, más que hacia si será necesario hacerlo. Esta evolución, unida a la reciente actuación de las autoridades japonesas en defensa de la moneda, está contribuyendo a limitar las presiones bajistas sobre el yen. Tras la decisión, el USD/JPY mostró una reacción relativamente contenida, una señal que algunos operadores interpretan como una muestra de que el mercado es cada vez más reticente a volver a poner a prueba los niveles que anteriormente desencadenaron intervenciones oficiales. La combinación de medidas directas en el mercado, mensajes de apoyo por parte de responsables internacionales y una actitud más vigilante del Banco de Japón está elevando el coste de mantener posiciones excesivamente cortas de yenes. De cara a las próximas semanas, la evolución del tipo de cambio seguirá siendo un factor clave para la política monetaria japonesa. Un nuevo episodio de debilidad significativa del yen podría acelerar las expectativas de subidas de tipos, especialmente si coincide con unos datos macroeconómicos estadounidenses que mantengan la presión sobre los diferenciales de rentabilidad entre ambos países. La reunión del BoE dejó una sensación menos acomodaticia de la que descontaba parte del mercado. Aunque los tipos permanecieron inalterados en el 3,75%, la votación mostró una división significativa dentro del comité, con un resultado de 6-3 a favor de mantener los tipos y tres miembros defendiendo una subida inmediata de 25 pb. El hecho de que el número de votos a favor de endurecer la política monetaria aumentase respecto a la reunión anterior fue interpretado por el mercado como una señal de creciente preocupación por los riesgos inflacionistas.

El mercado de ayer

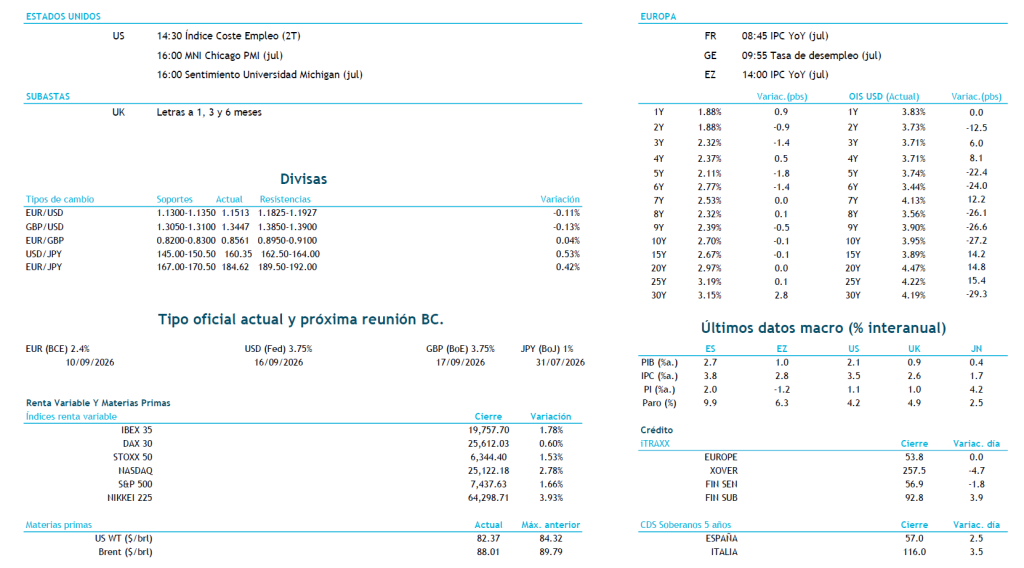

ES La inflación en España repuntó al 3,5% interanual en julio (vs. 3,2% esperado y 3,2% anterior)

EZ La inflación alemana también sorprendió al alza reforzando las presiones de precios en la Eurozona

GE El PIB de la Eurozona en el 2T mostró un crecimiento resiliente, apoyando la narrativa de una economía que resiste mejor de lo previsto pese al entorno geopolítico adverso.

US Los ingresos personales aumentaron un 0,2% en junio, mostrando una moderación frente al mes anterior, mientras que el Core PCE avanzó solo un 0,1% mensual y se desaceleró al 3,3% interanual, una señal favorable para la inflación; además, las reclamaciones continuas de desempleo se mantuvieron en niveles reducidos, reflejando un mercado laboral todavía sólido.

Resumen del mercado

El presente documento ha sido preparado por CECABANK S.A. únicamente con fines informativos y no debe ser considerado como ningún tipo de oferta, ni como una invitación a que le hagan ofertas, ni como una solicitud recomendación tendente a la formalización de una operación, ni como una aceptación formal o informal de los términos de una posible operación. Sin perjuicio de que la información aquí contenida refleje posibles términos y condiciones contractuales bajo los cuales podría ser estructurada una operación, no se asegura que la operación pueda ser finalmente formalizada, y los mismos no suponen en ningún caso obligación alguna por parte de CECABANK S.A. en cuanto a la formalización de la operación. CECABANK S.A. ha enviado el presente documento en su condición de posible contraparte de operaciones mercantiles entre profesionales. CECABANK S.A. no está actuando como su asesor jurídico, financiero, fiscal o contable, ni como su representante o mandatario, en relación con los términos y condiciones de la posible operación arriba indicada, ni en relación con cualquier otra operación a no ser que así haya sido acordado por escrito. Antes de formalizar cualquier operación deberá asegurarse de que entiende perfectamente el contenido de la misma y de que ha realizado una valoración independiente, sobre la base de su propio criterio y del asesoramiento de los expertos que estime conveniente, de la adecuación de la operación a sus objetivos y circunstancias, teniendo en cuenta los posibles riesgos y beneficios de la misma tras su formalización, así como sus implicaciones fiscales, incluida la obtención del asesoramiento fiscal correspondiente.